Introduction to the UAE Landscape

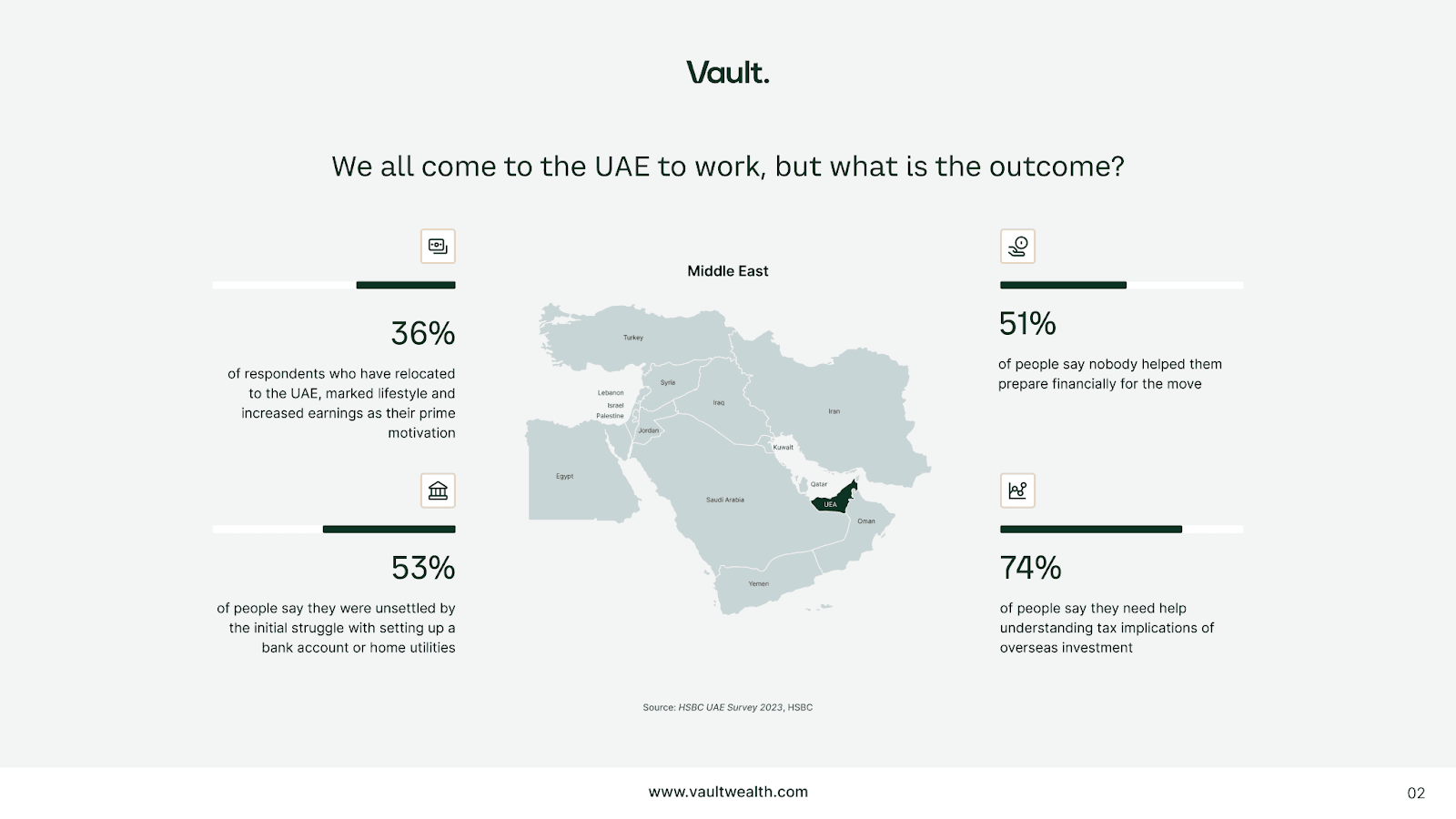

In the diverse landscape of the UAE, where economic opportunities abound and a tax-free environment prevails, retirement takes on a unique dimension. For many expatriates living in the UAE, retirement is not just about ceasing work; it’s about attaining financial independence, allowing them to pursue their passions without worrying about meeting their desired lifestyle. However, although most initially arrive intending to save and build wealth, most end up delaying their saving efforts. The diagram below illustrates some of the many challenges faced by UAE expats.

Source: HSBC UAE Survey 2023

Many expats also fall into the trap of excessive spending without consciously considering the impact on their savings goals.

A roadmap for expats

Define your end goal

Start by envisioning your retirement: your location, lifestyle, and income needs. This clarity will serve as the foundation for creating a financial plan that bridges the gap between your current situation and your future aspirations. With the high cost of living in the UAE, it’s crucial to have a well-defined financial objective.

Build an emergency cash fund

Establish an emergency cash fund equivalent to six months of expenses, including any planned major purchases. This fund acts as a safety net to handle unexpected expenses and provides the confidence needed to enter the world of investing, which is a crucial aspect of achieving financial independence.

Diversify your investments

Diversification is your best defense against risk. Allocate your investments across various income-generating assets like diversified company ownership (equities), real estate, and lending (bonds or sukuk). This strategy reduces risk and creates multiple income streams, safeguarding your financial future.

Consult a reputable financial advisor

Seek guidance from a reputable financial advisor who is competent, ethical, and client-focused. A good advisor will help you assess your financial situation, identify your goals, and create a customized plan to achieve them. They will also prioritize cost-effective investment implementation, provide behavioral coaching to navigate emotional investment decisions, and assist in formulating withdrawal strategies that maximize your portfolio’s longevity.

Embrace the emotional journey of investing

Remember that investing is not only a financial endeavor but an emotional one as well. Keep your long-term goals at the forefront when reviewing your portfolio. Your decisions today should align with the fundamental reasoning of your future aspirations.

Maintain consistency in saving and investing

Start saving and investing early and remain consistent. Even small, regular contributions can accumulate over time due to the compounding effect, leading to substantial wealth accumulation. The sooner you begin, the better equipped you are to achieve your financial goals.

UAE-specific considerations

The UAE offers expatriates numerous economic opportunities in a tax-free environment. A timeless strategy for wealth accumulation is to concentrate risk early in life by specializing in a career or focusing on building a business to create a substantial pool of wealth. As your wealth grows, it’s essential to diversify your assets to ensure preservation over extended periods.

Conclusion

In the UAE, the path to financial independence is laden with opportunities, but it also demands careful planning and strategic decision-making. Exploring these steps, with the help of a good financial advisor, can pave the way for a financially independent future in this dynamic and promising environment.

Frequently asked questions

What's the realistic timeline to financial independence in the UAE?

20-30 years from start to genuine independence for most professionals saving 20-30% of gross income and investing in a globally diversified portfolio. Higher savings rates compress the timeline materially — at 40-50% savings, the timeline drops to 12-17 years.What savings rate should I target?

At minimum 20% of gross income; ideally 25-30% for HNW professionals with surplus capacity. The UAE's zero-income-tax environment makes high savings rates more achievable than in heavily taxed jurisdictions — make use of the structural advantage rather than scaling lifestyle to consume it.What's the safe withdrawal rate in retirement?

The widely-used 4% rule (saving 25x annual spending need before retirement) is a useful starting point. For UAE expats expecting a multi-decade retirement, a slightly more conservative 3.5% is often the right anchor — building in tolerance for longer lifespan and sequence-of-returns risk.What about my End-of-Service Gratuity?

Treat it as a supplementary lump sum, not as the foundation. The gratuity was designed as severance, not retirement — for a HNW professional, it typically represents 1-2 years of living expenses, not 20-30.

Related reading

More on Wealth planning

- InsightThere Is No Such Thing as a Guaranteed ReturnAn NRI scheme promising '17% guaranteed' is doing the rounds again. From leveraged FCNR deposits to 'capital-protected' notes and guaranteed rental yields, the word guaranteed is usually where the risk is hidden — here's how to read the fine print before you invest.

- InsightPlanning for Retirement When There’s No Pension: A Guide for Private Sector Employees Using Wealth ManagementMoving beyond simple savings: A guide to building a portable, diversified investment portfolio for retirement while work

- InsightBeyond the Algorithm: Why Human Advisors Still Matter in the Age of WealthtechDigital tools bring speed — but HNW investors in MENA still need trust and strategic advice. Explore why the future of wealth blends tech with human guidance.