Why Choose a ‘Good’ Financial Advisor?

In today’s complex financial landscape, choosing a good financial advisor can make all the difference when it comes to achieving your own financial goals. A skilled wealth manager can make a massive difference in your asset allocation, implementing your investments cost-effectively, overcoming your emotional biases, investing tax-efficiently, and coming up with sound withdrawal strategies. However, it is crucial to emphasize the importance of the word “good” in the context of financial advisors, as not all of them prioritize your best interests. In the following article, we’ll dive into the most important ways a “good” financial advisor can help you make the most of your wealth, as well as the pitfalls of ending up with the wrong one.

The Importance of Choosing a Good Financial Advisor

We can’t overstate how important it is to select a financial advisor who is competent, ethical, and truly focused on your needs. A poor choice can lead to mis-selling, where advisors prioritize their commissions over your own best interest, resulting in potentially significant financial losses. This issue has plagued regions like the UAE, where many individual investors have lost confidence in the financial advisory industry due to the prevalence of unscrupulous practices and unaligned incentives. A prime example of this is the widespread promotion of ‘Whole of Life Insurance’ in the UAE, where the advisory firm makes a heavy upfront fee from the insurer to conduct the sale. In a majority of cases the policies are sold to clients seeking investments for their long-term future rather than an insurance policy.

To avoid falling victim to such advisors, it is essential to conduct thorough research and due diligence before entrusting your finances to a professional. Look for advisors with strong credentials, transparent fee structures, and a solid track record of prioritizing their clients’ interests. You can do so by taking a second opinion to ensure consistency of advice, asking for testimonials, and most importantly question any advice given to ensure it is in your best interest and not theirs.

Asset Allocation and Portfolio Construction

A knowledgeable financial advisor understands the importance of a well-diversified investment portfolio tailored to your individual goals, risk tolerance, and time horizon. They can help you choose the right mix of asset classes that align with your objectives, and continuously monitor and adjust your portfolio to keep it on track.

Cost-Effective Implementation

Financial advisors can help identify and utilize low-cost, high-quality investments that minimize expenses, which can have a significant impact on your long-term returns.

Behavioral Coaching

We’d go so far as to say that the most underrated and valuable service a financial advisor can offer is behavioral coaching. They can help you navigate the emotional roller coaster of investing by providing objective guidance and preventing you from making impulsive decisions driven by fear or greed. This coaching can ultimately lead to better long-term investment outcomes.

In March 2020, in the midst of COVID, we saw many investors sell their investments due to the environment of lockdowns and the fear of the unknown. Many advisors had advised this approach to try to take advantage of the uncertainty in the market. This turned out to be a very terrible approach as the bottom of the market happened to be in March 23, 2020 which was peak-fear in the market. From March 23rd till end of year, the S&P500 gained a staggering 45%. A good advisor can have a significant impact by giving tough advice in the most important of times.

Goal Identification and Goal-Based Planning

Every individual investor has unique circumstances and objectives that should be taken into account when developing a financial plan. A good financial advisor will work closely with you to identify your goals and create a tailored strategy to achieve them. This personalized approach ensures that your specific needs and aspirations are addressed, laying the groundwork for long-term financial success.

Withdrawal Strategies and Investment Approaches for Financial Independence

As you transition into retirement, a financial advisor can help you develop a withdrawal strategy that maximizes your portfolio’s longevity, guiding you on the optimal order of withdrawing from various account types based on your unique situation and financial goals. In addition, they can focus your portfolio allocation to be in both dividend and non-dividend paying companies, whilst still generating your desired income generation through timely withdrawals; this ensures you maintain a well-diversified portfolio that supports you in years to come.

Conclusion

In a world of ever-changing financial markets and evolving personal circumstances, a good financial advisor can be an invaluable partner in helping you achieve your financial goals. By focusing on areas within their control, such as asset allocation, cost-effective implementation, and tax-efficient investing, they can add significant value to your wealth management strategy. Moreover, their expertise in behavioral coaching and retirement withdrawal strategies can lead to better long-term outcomes and peace of mind.

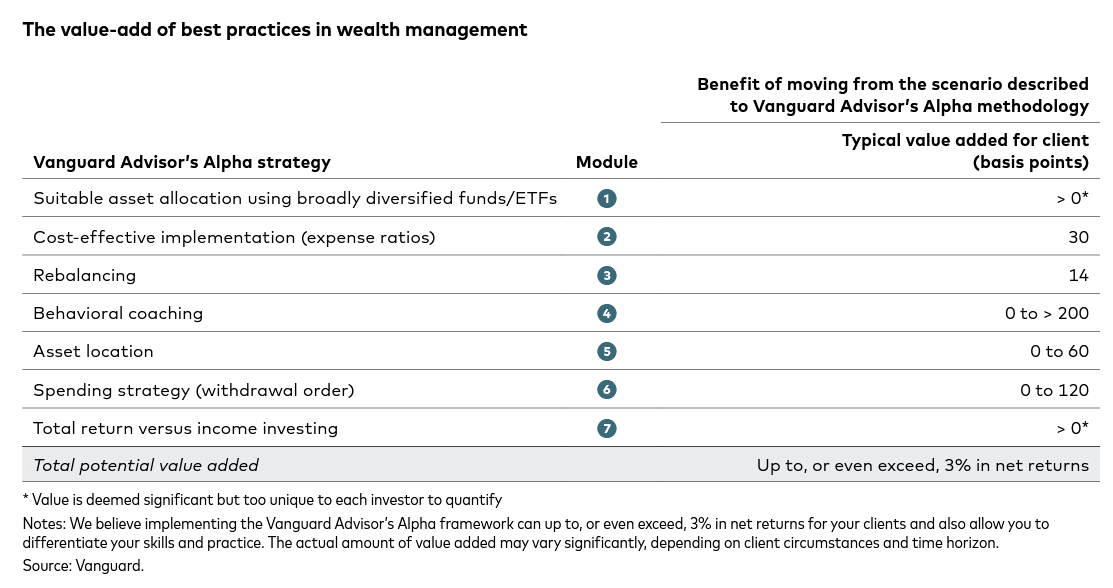

Final note: a good financial advisor shouldn’t cost you anywhere more than 1% per annum. However if we were to quantify the added value it would definitely exceed this cost. Vanguard, the pioneer in passive investing, go as far as quantifying the value-add as a figure that can exceed 3% in net returns.

Source: Vanguard

Frequently asked questions

What does a good financial advisor actually do?

Five concrete things: (1) Sets a diversified asset allocation tailored to your goals, risk capacity and time horizon; (2) Implements it cost-efficiently using low-cost vehicles and clean execution; (3) Coaches you through behavioural biases — the panic-sell, the FOMO buy, the over-trading impulse; (4) Optimises for tax efficiency across jurisdictions and account types; (5) Designs a withdrawal strategy when you eventually start drawing income.How do I identify a bad advisor?

Three red flags. Commission-driven compensation (especially insurance-linked products presented as investments). Opaque fee structures where the actual annual cost is hard to determine. Pressure tactics — urgency, scarcity, exclusivity language designed to push you into a decision before you've checked the structure.What's wrong with whole-of-life insurance being sold as an investment?

Whole-of-life contracts (Zurich Futura, MetLife Future Protect, etc.) generate large upfront commissions for the seller — sometimes 7-10% of the first year's premium — and lock the customer into high ongoing charges, illiquid structures and severe surrender penalties. They're insurance products that occasionally make sense for genuine insurance needs, but they're almost always the wrong choice when an investment outcome is the actual goal.How do I verify an advisor's credentials in the UAE?

Check the regulator's public register: FSRA (fsra.adgm.com) for ADGM firms, DFSA (dfsa.ae) for DIFC firms, SCA (sca.gov.ae) for onshore-UAE firms. Verify individual advisor accreditations (CFA, CFP, etc.) with the issuing body. Ask for client references — a genuine fiduciary will provide them.Is the fee for a good advisor worth it?

Generally yes, in two scenarios. Complex situations — cross-border, multiple income sources, business interests, succession planning — where bad decisions are expensive and good decisions are non-obvious. Behavioural risk — you suspect you'd panic-sell during a 30% drawdown or over-trade during a bull market. A good advisor often pays for itself in a single major decision they help you make or avoid.

Related reading

More on Wealth planning

- InsightThere Is No Such Thing as a Guaranteed ReturnAn NRI scheme promising '17% guaranteed' is doing the rounds again. From leveraged FCNR deposits to 'capital-protected' notes and guaranteed rental yields, the word guaranteed is usually where the risk is hidden — here's how to read the fine print before you invest.

- InsightPlanning for Retirement When There’s No Pension: A Guide for Private Sector Employees Using Wealth ManagementMoving beyond simple savings: A guide to building a portable, diversified investment portfolio for retirement while work

- InsightBeyond the Algorithm: Why Human Advisors Still Matter in the Age of WealthtechDigital tools bring speed — but HNW investors in MENA still need trust and strategic advice. Explore why the future of wealth blends tech with human guidance.