Overview

For over a year now, the anticipation and movement of interest rates has been the key factor influencing markets. The reason for this recent bout of fluctuations in interest rates is closely tied to inflation, which has been a major economic and political concern around the world.

In this series of email memos, we will explore the various factors that are driving inflation (both in the short and long-term). These include:

- Supply chain disruptions

- Globalization

- Quantitative easing/tightening

- Technology

This topic is way too long to write in one newsletter, and therefore will be splitting this one up in parts. To start, let’s first focus on the most recent and relevant aspect driving inflation, which is a mismatch between supply and demand.

Supply Chain Disruption

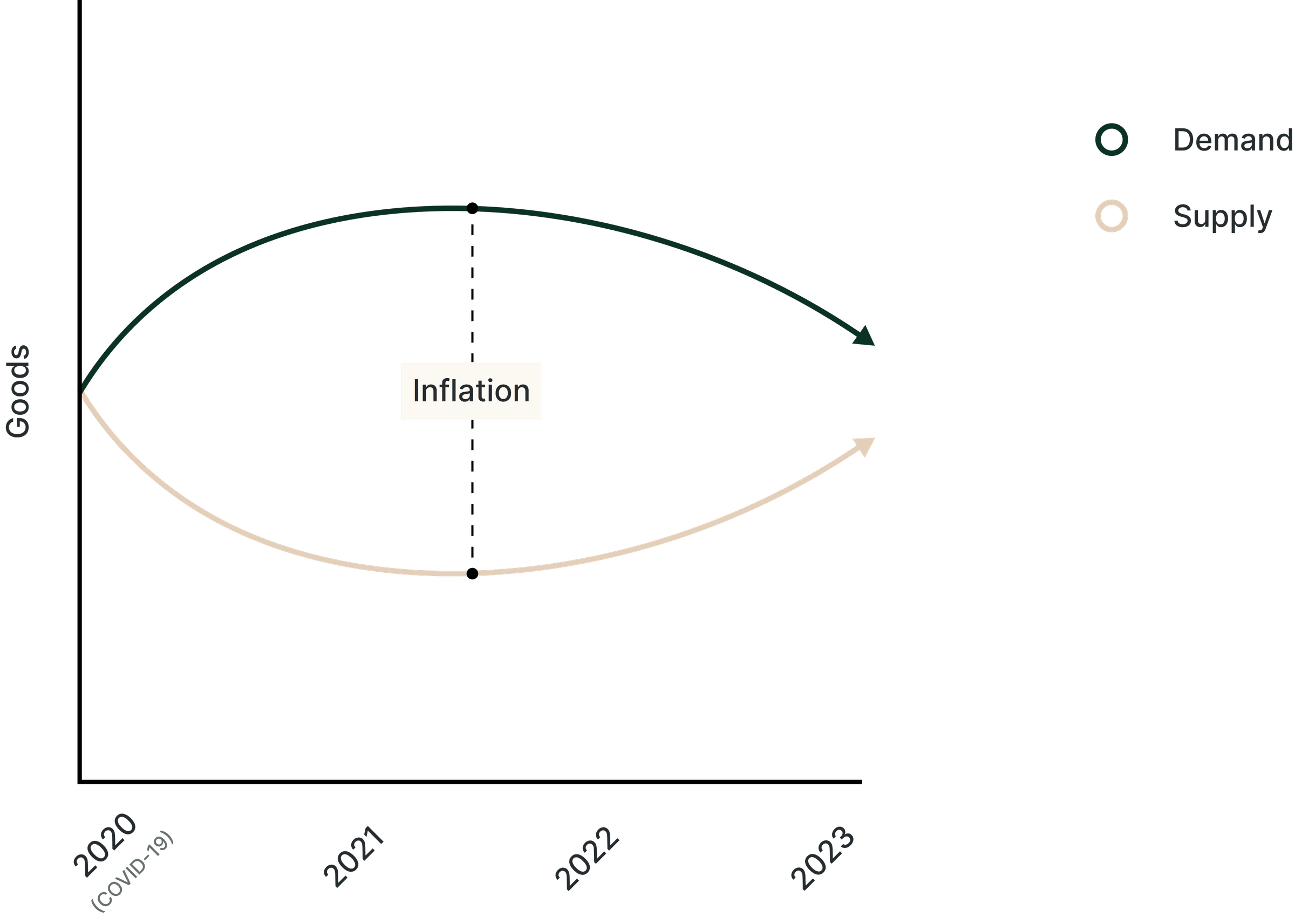

Early on in 2020, the very onset of COVID was a shock to everyone and everything, including production markets no less.The uncertainty of how the world was changing that year forced a drastic shift in focus and behavior for both consumers and businesses.

During that time, our guess is you likely spent much less on hospitality and other in-person services. The money we had all stopped spending on services, however, wasn’t entirely all saved; instead, there was a massive jump on spending on goods.

To give you an idea, data from the Peterson Institute shows that Q4 spending in 2020 was up 11.9% for durable goods (and 4.3% for non-durables). Meanwhile, expenditure on services was down 6.8%, with overall consumption going down by only 2.4%.

This visible shift in demand sparked a disruption in the supply chain, causing businesses to struggle to keep up with the sudden increase in demand for goods. Since many companies were not prepared for this sudden change, having to quickly adapt their production processes led to shortages of certain products, causing an increase in prices for goods.

To add to that, the supply chain disruptions were further exacerbated by the lockdowns and travel restrictions; many factories had to close down temporarily, leading to a reduction in production and logistics delays across the board.

Normally, supply and demand imbalances eventually resolve themselves over time. On one hand, as restrictions were lifted, the shift away from goods and back to services helped ease the excess demand for goods. However, just as supply and demand were starting to return to a normal balance, the onset of the war between Russia and Ukraine had a significant impact on commodity and energy prices, disrupting the global supply chain even further.

Recovery

Despite these challenges, supply chains tend to adapt and recover as time passes. As buyers shift their sourcing to other vendors, and sellers look to new markets, the balance begins to restore itself. When these supply chains eventually stabilize, we can expect to see the inflationary pressures ease. It’s important to note that mismatches between supply and demand are typically short-lived when it comes to inflation, as the market eventually adjusts to a new equilibrium.

Conclusion

In line with the insights of Matt Ridley in The Rational Optimist: How Prosperity Evolves, it’s become pretty clear that innovation and the functioning of free markets play a crucial role in correcting supply-demand imbalances and stabilizing prices as well. When a particular good is in shortage, entrepreneurs are incentivized to implement new technologies or production methods to enhance said supply, thereby helping bring prices back to equilibrium. Finally, it is worth noting that as prices rise, the likelihood of price stability also increases given its decreased demand due to being less affordable.

Frequently asked questions

What caused the recent inflation spike?

A combination of demand and supply shocks. Demand: COVID lockdowns shifted household spending sharply from services toward physical goods. Supply: factory closures, port congestion, and shipping bottlenecks meant capacity couldn't expand to meet that demand. Prices for goods rose first, then services followed as labour markets tightened.Is this kind of inflation temporary or permanent?

Supply-shock inflation tends to be self-correcting once capacity catches up — which is largely what's played out through 2024-2026 as supply chains normalised. The structural picture (globalization, technology, monetary policy) matters more for where inflation settles in the long run.Why did goods inflate before services?

Because the demand shift was toward physical goods (durables — appliances, electronics, home improvements) and supply for goods is more constrained by physical capacity. Services capacity is more elastic — restaurants reopened and prices adjusted with a lag.What does this mean for portfolios?

Supply-driven inflation is bad for nominal bonds and ambiguous for equities (firms can pass costs through but margins compress). It's particularly favourable for real assets and pricing-power businesses. The fix isn't to time the shock — it's to hold a diversified portfolio that doesn't depend on stable prices to generate real returns.

Related reading

More on Markets & macro

- InsightInflation Part 4: Monetary Policy and the Future of InflationPredicting future inflation trends.

- InsightInflation Part 03: TechnologyHow technology is the most significant factor in the inflation story.

- InsightInflation Part 02: GlobalizationDeep dive into some of the critical ways that globalization has contributed to a low inflationary environment.