Overview

In Part 1 of our inflation series, we discussed how disruptions in supply and demand can have a significant short-term impact on inflation, which became a strong reality after the onset of COVID-19 and the war in Eastern Europe. In Part 2, we explored how globalization has historically driven deflation and whether the political environment indicates that this trend is ending. In Part 3, we’ll examine how technology has transformed production and, in turn, prices of goods, making it the most significant factor in the inflation story.

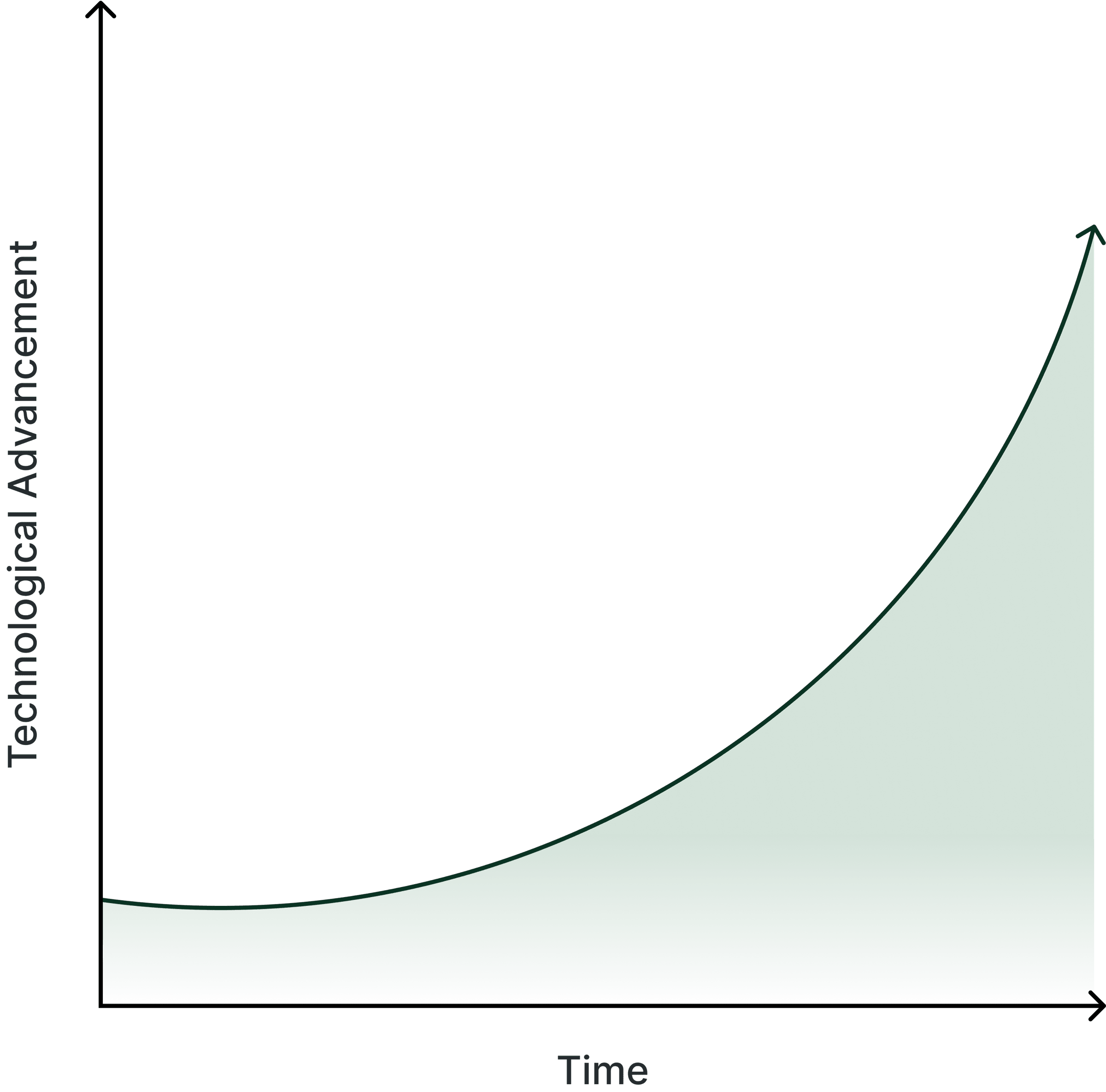

It cannot be understated how much technological progress has driven economic growth since the Industrial Revolution. As technology advances, production efficiency improves, leading to lower costs of goods and services. Fierce competition in the market further drives prices down, creating a desirable form of deflation that allows societies to consume more for less; this ends up freeing up resources for other specialized areas of production across the board.

Moore’s Law

Let’s look at the semiconductor industry as one example of this trend. Over the past several decades, the cost of producing a single transistor has decreased by a factor of a billion, contributing significantly to technological advancement and economic growth.

Now, we cannot talk about technological advancement without mentioning Moore’s Law. This law predicts that the number of transistors on a microchip doubles approximately every two years, meaning the speed and capability of our computers hugely increase every two years as well. The key point here is that we’ll be paying less to consume more advanced technologies. Currently, technology is transforming traditional business practices in areas such as virtual meetings, chatbots, clean energy/fusion, and more. Sam Altman, CEO of OpenAI (the company behind ChatGPT), speaking of artificial intelligence has stated that the costs of intelligence and energy are going to be on a path towards near-zero.

This trend is very likely to continue, with technological advancements leading to even greater production efficiency gains and more deflationary pressure on prices. Although the short-term impacts of COVID-19 and the war in Eastern Europe have been severe, this long-term trend is one that will ultimately reduce inflation.

Conclusion: Other Considerations

With all of this in mind, a long-term deflationary trend due to production advancements also has its downsides, as hoarding cash becomes a preferred strategy. If prices of goods and services are declining, then holding cash seems like a sound long-term wealth management strategy. This approach tends to have a strong negative impact on economic growth, as hoarding cash prevents investment in further production through lending and ownership. As such, this is why central banks target a small (and seemingly valuable) positive inflation rate, a topic we’ll dive into in the final part of our inflation series covering monetary policy.

Frequently asked questions

How much has technology actually reduced prices?

Pick any tech-intensive category — computing, storage, telecommunications, solar power — and you'll find cost curves that have fallen by 10x to 1,000x over a generation. A single transistor today costs a billionth of what it did in the early days of integrated circuits. This is the engine behind the productivity gains in essentially every part of the modern economy.Will AI continue this trend?

Almost certainly yes — and likely accelerate it. AI compresses the cost of cognitive work (research, drafting, coding, customer service) the way the steam engine compressed the cost of physical work. The implication for prices: anything that's currently expensive because it requires human attention gets cheaper, faster than most forecasters expect.Is deflation a good thing or a bad thing?

Productivity-driven deflation is good — it means consumers get more for less and resources free up for new production. Demand-collapse deflation is bad — it triggers liquidity traps and cascading defaults (the Great Depression dynamic). Central banks fight the second kind, sometimes at the cost of dampening the benefits of the first.What does technology deflation mean for portfolios?

Two things. First, own the businesses driving it — productivity-leading companies typically compound earnings faster than the broader economy. Second, under-weight the businesses being disrupted — categories where AI or automation can replicate the value proposition at a fraction of the cost. The next decade will likely see meaningfully wider winner-loser gaps than the last.

Related reading

More on Markets & macro

- InsightInflation Part 4: Monetary Policy and the Future of InflationPredicting future inflation trends.

- InsightInflation Part 02: GlobalizationDeep dive into some of the critical ways that globalization has contributed to a low inflationary environment.

- InsightInflation Part 01: An Unfortunate Mismatch between Demand & SupplyIn this series of email memos, we will explore the various factors that are driving inflation (both in the short and lon