Introduction: USD Losing its Reserve Currency Status

We have received numerous questions from investors about the news of the USD potentially losing its reserve currency status due to emerging market economies agreeing to transact directly without the dollar intermediary. Therefore, we share a few reasons why you should not worry about this.

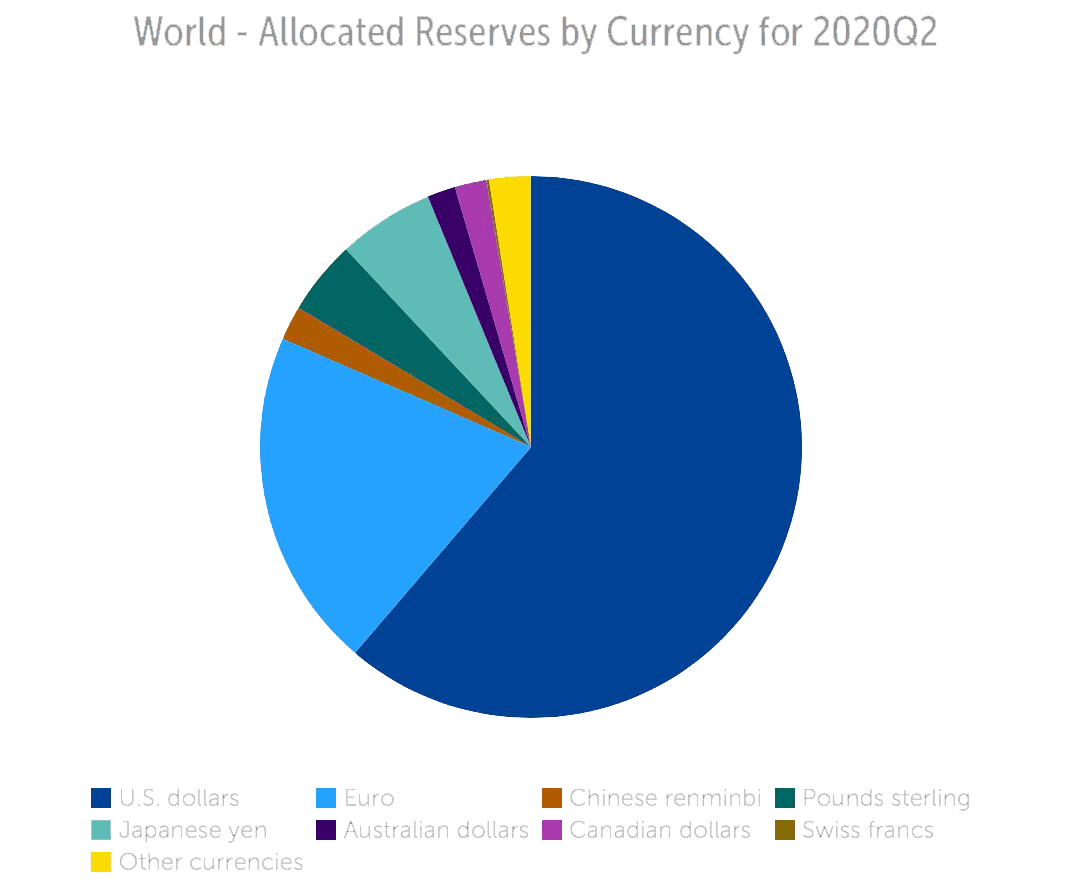

Global Currency Share

Firstly, according to the International Monetary Fund (IMF), the U.S. dollar still comprised approximately 58% of global foreign exchange reserves in the fourth quarter of 2022, while the Euro, the second most widely held reserve currency, accounted for roughly 20%. The substantial gap between the USD and its closest competitor demonstrates the dollar’s entrenched position in international finance.

Settling Trade

Secondly, the U.S. dollar is the primary currency for invoicing and settling international trade transactions. The Bank for International Settlements (BIS) estimates that about 40% of global trade is still invoiced in USD. This widespread use of the dollar in global trade creates persistent demand for the currency, further solidifying its status as the dominant reserve currency.

Yuan vs. USD

Thirdly, much has been said about Chinese holdings of U.S. federal debt. It’s important to acknowledge that China owns less than 4% of the debt. Their purchase of this debt, through their substantial holdings of U.S. Treasury bonds, has played a vital role in maintaining the country’s competitive edge in international trade. By accumulating large amounts of U.S. Treasuries, China effectively keeps the value of its currency, the yuan, relatively low compared to the U.S. dollar. A weaker yuan boosts China’s exports by making them more affordable for foreign buyers, contributing to its trade surplus. If China significantly reduced its holdings of U.S. Treasuries, it would lead to an appreciation of the yuan against the dollar, making Chinese exports more expensive and less competitive in international markets. Consequently, China has a vested interest in maintaining the status quo, as a strong U.S. dollar benefits its export-driven economy. This interdependence between the U.S. and China adds another layer of stability to the dollar’s role as the world’s primary reserve currency and further underscores the challenges in replacing the dollar in the global financial system.

USD Stability

Lastly, while it is true that emerging market economies are increasingly exploring alternatives to the U.S. dollar for trade and financial transactions, the transition away from the dollar’s reserve currency status is likely to be a slow and gradual process. The existing infrastructure, liquidity, and stability provided by the U.S. financial markets, along with the deeply entrenched position of the dollar in international finance, will not be easily supplanted.

Conclusion: Other Remarks

However, regardless of all this talk, holding USD in a bank account is not a sound wealth management strategy. Cash is designed to lose value over time. We recommend that cash only be held as an emergency cash fund —this includes the cash you may need in an emergency, as well as a reserve of what you know you will definitely be spending above what your income can afford you in the next 2 to 3 years (e.g., a house purchase that you know you’ll be making next year).

Ownership of real assets has always been the solution to a surplus of cash, which includes the ownership of companies. Equities are the best option to own real assets, as they provide the ability to heavily diversify your ownership and its accompanying risks. By owning a diversified portfolio of company ownership, you own the production of these assets. Even though this production is currently in USD, you own the production regardless of the currency it is being sold in. Should the USD lose value, the earnings go up as the prices of production do too.

The devaluation of currency through inflation is a nudge for holders of wealth to put their funds to use in owning productive assets. In essence, investors must focus on owning real assets rather than hoarding cash, as this will better protect their wealth in the long run.

Frequently asked questions

Is the USD's reserve-currency status really at risk?

The pace of change is gradual, not sudden. The USD's share of global reserves has declined from roughly 70% to around 58% over two decades. The replacement isn't a single competitor — it's diversification across the Euro, Yen, RMB, and gold. The USD remains structurally dominant by most measures.What would a meaningful de-dollarisation look like?

Central banks reducing USD holdings by tens of percentage points over a decade, alongside material growth in non-USD pricing of major commodities (oil, copper, wheat) and non-USD denomination of global trade contracts. Both are happening at the margin but not at scale yet.Should this affect my portfolio?

Modestly. Maintaining diversification across major currencies (which a globally diversified equity portfolio naturally provides) is the right answer. Concentrated bets on de-dollarisation (gold maximalism, RMB-denominated assets) typically underperform broad diversification over multi-decade periods.

Related reading

More on Cash & savings

- InsightMaximise Your Savings Returns in the UAE — Strategies for 2026Practical strategies for getting more out of your AED and USD savings in the UAE in 2026 — high-yield accounts, FX, and where cash hurts a wealth plan.

- InsightWhy Your Idle Dirhams are Losing 4% Every YearIdle cash in the UAE is losing value to inflation. Learn how a private wealth management service in Dubai can move you from savings to active investment.

- InsightBest High-Yield Savings Accounts in the UAE — 2026 GuideA comparison of the top AED and USD high-yield savings accounts in the UAE for 2026 — interest rates, minimum balances, fees, and how Vault SmartCash stacks up.