Introduction

Over the past two years, we have gotten accustomed to short interest rate movements and inflation expectations, which often move together and are the primary drivers of stock, bond, and all other asset price movements. The mass market decline was driven by high inflation and massive interest rate increases. This decline was then stabilized by inflation cooling off and showing a trend back to normal.

However, the equity market has since rallied back to all-time highs regardless of interest rates remaining high. This proves that there is now a stronger force driving asset prices, particularly that of company ownership (i.e., equities).

On Wednesday, the Federal Reserve (the US central bank that determines short-term interest rates) announced that they would keep interest rates at the current level of between 5.25% and 5.50% and maintained its expectations of three cuts through the year to 4.50% to 4.75%. However, they also indicated that there would be expectations of fewer cuts in 2025 and 2026 than was previously forecasted. However, stock prices remain at all-time highs, which has been concerning for many investors.

So what is happening, and why are many investors confused about what drives equity prices? Lets deep dive into this.

Factors Affecting Equity Prices

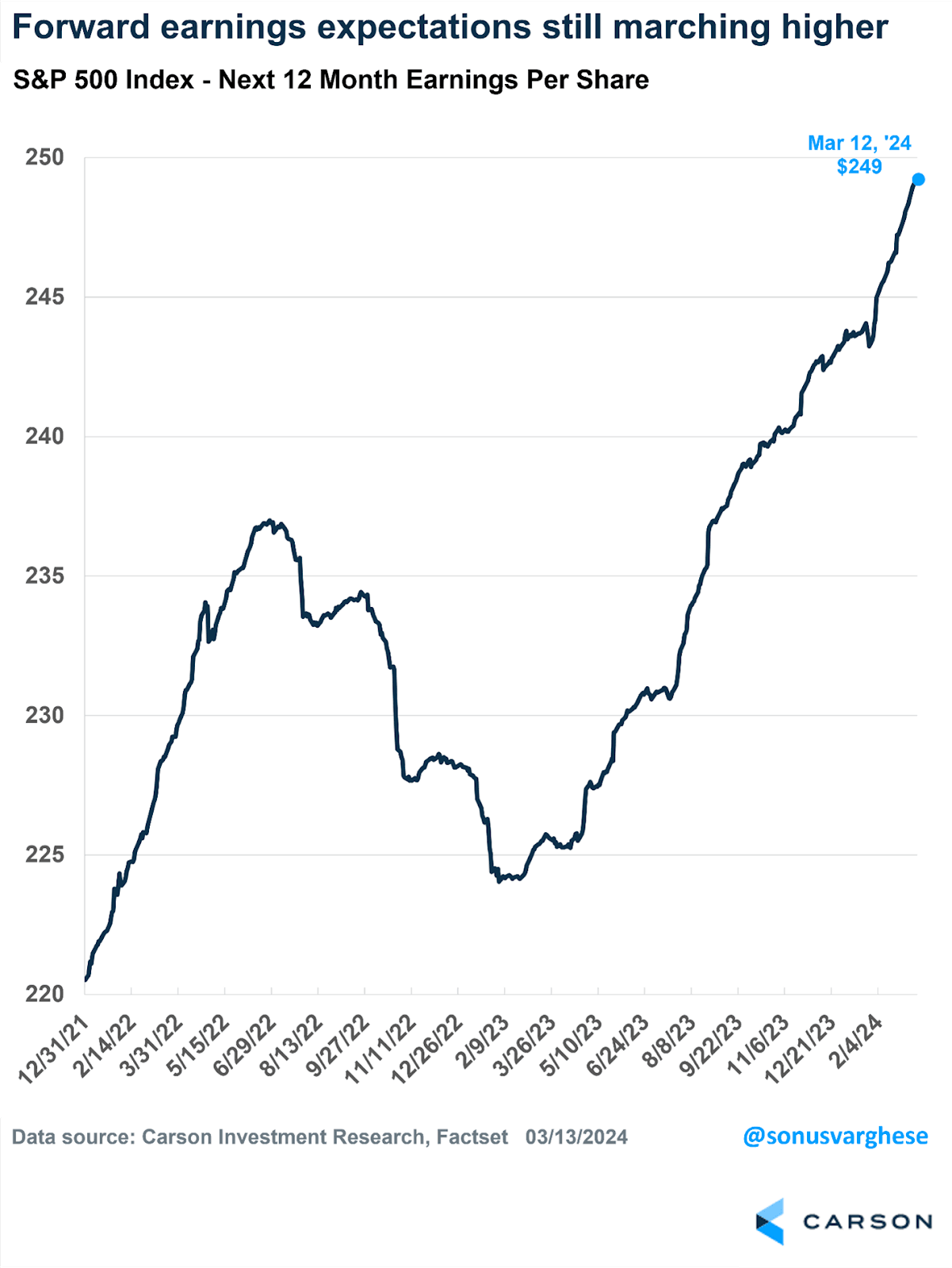

When we buy any company(s), whether private or publicly listed, the primary motivator is buying earnings and companies’ future earnings. A significant note is that corporate earnings are at their highest level in history, even in an environment where interest rates moved from 0% to north of 5% within a short period. Earnings have continued to rise with profit margin increases and revenue growth. The Fed also boosted its expectations for GDP growth, which indicates that the economy’s production capacity is growing.

Source: Carson Investment Research

See the above chart, which shows forward expectations for increasing earnings.

Of course, company values will go up. They are making more money than they ever have, and there is an expectation that they will continue to grow at a fast pace.

When investing in bond markets, our expected return is the return we are contractually promised to receive throughout the lending agreement. With high interest rates, these are attractive.

However when investing in equities, our expected return is simply the earnings we are getting as owners of companies in addition to the earnings growth we receive over long durations. The earnings growth is a by-product of two key aspects:

- Growth in companies’ ability to generate profit through lower operating costs and higher revenue generated from a larger economy.

- Inflation, as companies’ costs go up, so do they increase their prices. That’s how we as consumers experience inflation: by the cost of the goods and services these companies provide going up, so do their earnings.

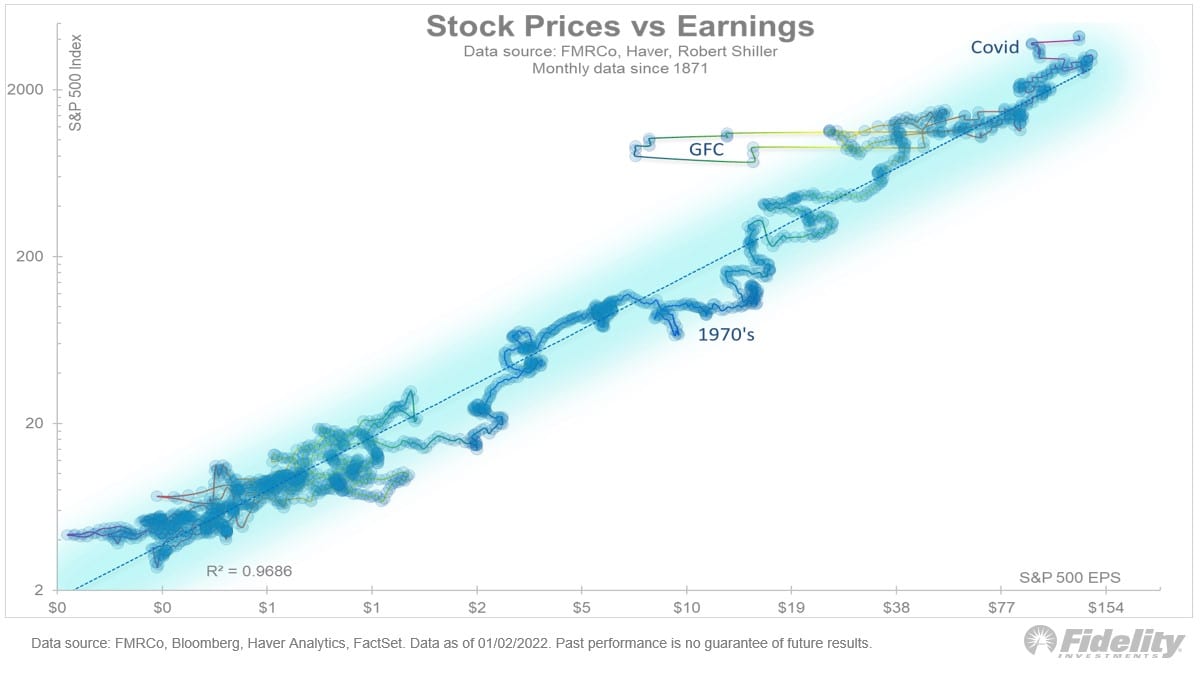

See below a great chart showing the high correlation between earnings and stock prices, proving that earnings growth, which includes both factors mentioned above, is indeed the primary force of equity market growth.

Source: Fidelity

Our view on equity prices is that they are natural to be at all-time highs, as earnings are also at all-time highs and should most usually be at all-time highs. The average listed company pays out less than 50% of its earnings in dividends. That means that companies are growing not only by the growth of their earnings but also by the earnings that are not distributed as dividends but instead retained in their value.

Conclusion

Be diversified, keep the focus on the long term, and cut out short-term noise, and you’ll get a natural return based on the global production of goods and services we continue to need on a daily basis.

Frequently asked questions

Should I avoid investing at all-time highs?

No. Markets spend roughly 30% of trading days at all-time highs over long historical periods — so "wait for a pullback" typically means missing significant compounding. The right framing is to invest based on your plan and time horizon, not on price level.How important are individual Fed decisions?

Less than commentary suggests. The trajectory of Fed policy over multi-year periods matters; specific 25-bps decisions in any given meeting rarely change the long-term picture meaningfully. Long-horizon investors typically don't need to react to individual meetings.What about earnings season?

Earnings drive medium-term price action but get noisy in the short term. Track the trend across multiple quarters, not the reaction to any single print. Aggregate earnings growth is the primary driver of equity returns over multi-year periods.

Related reading

More on Markets & macro

- NewsletterWhat 2025’s Market Turbulence Is Teaching InvestorsResearch shows that investor behaviour — staying invested, rebalancing, avoiding reactive decisions — has more impact on outcomes than any single market call.

- NewsletterGold’s Surge and What It Could Mean for InvestorsGold prices are soaring to record highs, but is the rally sustainable? Explore what’s driving demand, the risks ahead, and gold’s role in a modern portfolio.

- NewsletterIs the AI Boom a Bubble, or Just the Beginning?AI valuations are soaring — but is it sustainable? Discover what's fuelling the hype, where risks lie, and how MENA investors can stay exposed and protected.