Introduction: Locking in Your Fixed Deposit

For many people, the main investment-related concern for 2023 has been the possibility of an upcoming recession. This has caused some anxiety about the safest way to invest, which makes it natural to want to hold onto cash in such an environment. Even though banks are currently offering fixed deposits that have a very high return for short-term deposits, it’s important to consider the disadvantages of locking in this return for a short amount of time only.

When the term of a fixed deposit comes to an end (i.e. it matures), investors must decide whether to reinvest in another deposit or invest elsewhere. This is when many may realize that interest rates are no longer as attractive as they were at the time of the initial deposit once markets have recovered. This is the reason why we’re seeing longer-term investments yielding less than shorter-term ones.

As it stands, the current trend is as follows:

- 1-year Yield: 4.78%

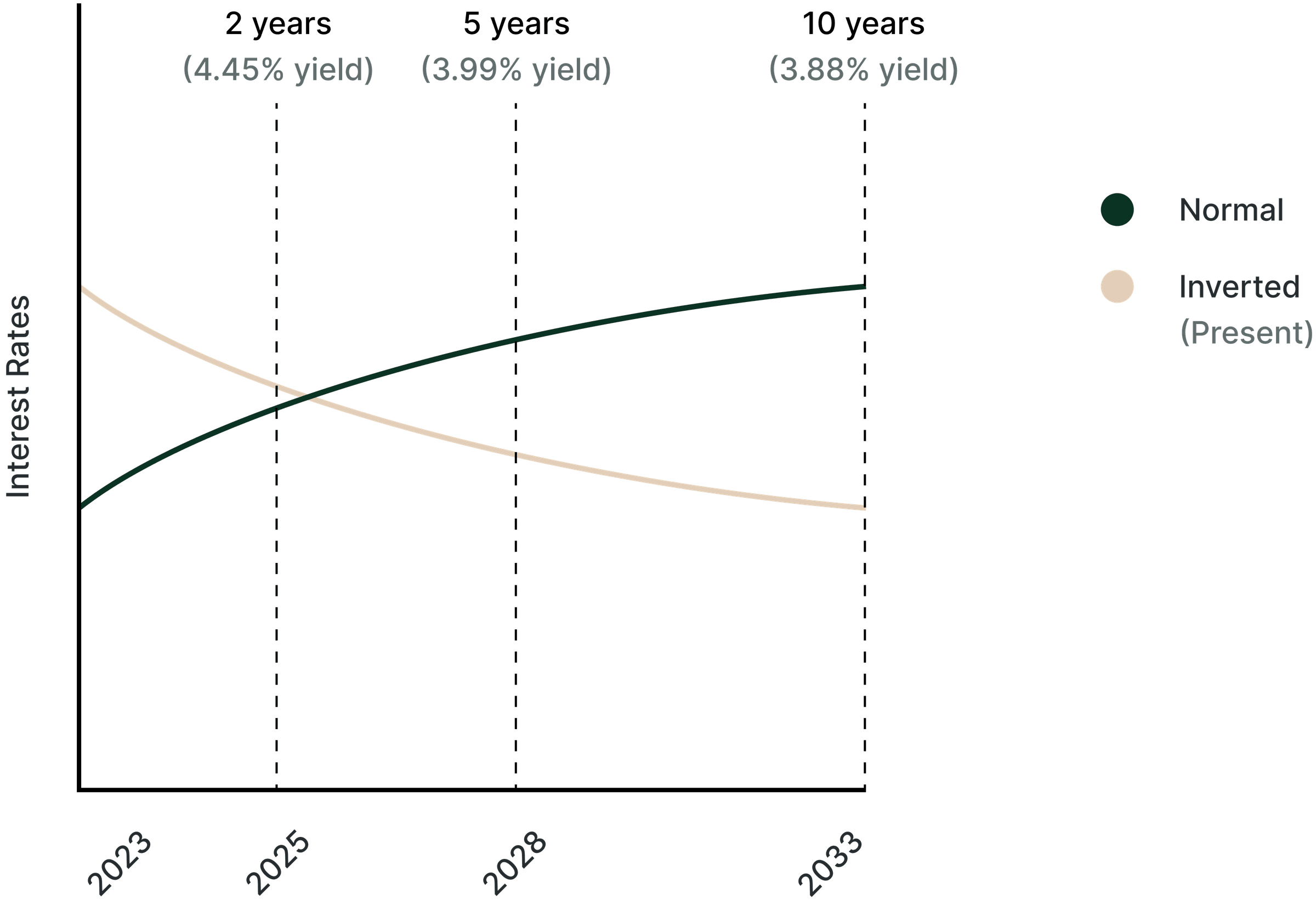

- 2-year Yield: 4.45%

- 5-year Yield: 3.99%

- 10-year Yield: 3.88%

The Inverted Yield Curve

This is known as an “Inverted Yield Curve”, where shorter-term rates are higher than those on longer-term investments. This phenomenon is unusual, as investors typically expect to earn a higher return for taking on more risk by committing their money for a longer period.

However, this atypical trend shows us that most high-value investors are currently willing to accept a lower return in exchange for the security of locking in their money for a longer period. These investors strongly expect that interest rates will eventually move back down. And in this case, investors will not be able to reinvest their savings down the road at a rate comparable to the current rate of return. With this in mind, investors are willing to take approximately 0.9% less return on locking their funds for ten years rather than one.

There are two main reasons investors expect interest rates to drop again:

- Many data points show that the recent burst of inflation is on a trajectory back to more normal levels. At the same time, the Fed (the central bank of the United States) is still planning to raise rates on the short term.

- An upcoming recession will very likely motivate the Fed to lower interest rates to support the economy.

All of this suggests that the fears many investors have about the upcoming recession have mostly been baked into current market prices. Also, it’s critical to remember that this concern is usually the primary indicator of interest rates dropping back down again in the future, which almost always leads to positive market performance down the road.

Conclusion: Moral of the Story

While it may be tempting to lock in a high return on a short-term investment, it’s important to consider the potential risk of reinvesting your money down the road at a lower rate. We encourage you to always carefully evaluate your investment choices based on your long-term financial goals.

Frequently asked questions

What is an inverted yield curve?

When short-term interest rates (e.g. 3-month Treasury) are higher than long-term rates (e.g. 10-year Treasury) — the opposite of the normal upward-sloping yield curve. Historically inversion has preceded most US recessions by 6-24 months, though not every inversion is followed by recession.Why does inversion predict recession?

Because the bond market is collectively betting that future short-term rates will fall — implying expectations of economic weakness ahead. The signal is reliable historically but the timing varies widely (sometimes immediate, sometimes 18+ months delayed).What should I do about it?

Lock in attractive long-end yields where your liquidity profile allows. The inverted curve means short-term cash pays more today but reinvestment at maturity will likely be at lower rates. A bond ladder extending into longer maturities can lock today's longer-rate yields — capturing optionality the inversion provides.

Related reading

More on Markets & macro

- NewsletterWhat 2025’s Market Turbulence Is Teaching InvestorsResearch shows that investor behaviour — staying invested, rebalancing, avoiding reactive decisions — has more impact on outcomes than any single market call.

- NewsletterGold’s Surge and What It Could Mean for InvestorsGold prices are soaring to record highs, but is the rally sustainable? Explore what’s driving demand, the risks ahead, and gold’s role in a modern portfolio.

- NewsletterIs the AI Boom a Bubble, or Just the Beginning?AI valuations are soaring — but is it sustainable? Discover what's fuelling the hype, where risks lie, and how MENA investors can stay exposed and protected.