Introduction: Market Shakeup

Market performance in 2022 has shaken up conventional investing practices, with media outlets particularly curious about the future of the 60/40 portfolio. To provide some context, a 60/40 portfolio is simply where an investor holds about 60% in equities and 40% in bonds (although these figures may vary).

Now, why invest in this type of portfolio in the first place? Firstly, holding equities long-term means consistent gains through company earnings and earnings growth due to economic growth and inflation. Secondly, holding bonds means receiving consistent earnings with less volatility. At the same time, bonds tend to perform well in a disastrous year where equities decline massively, which can create a more balanced and robust investment portfolio overall.

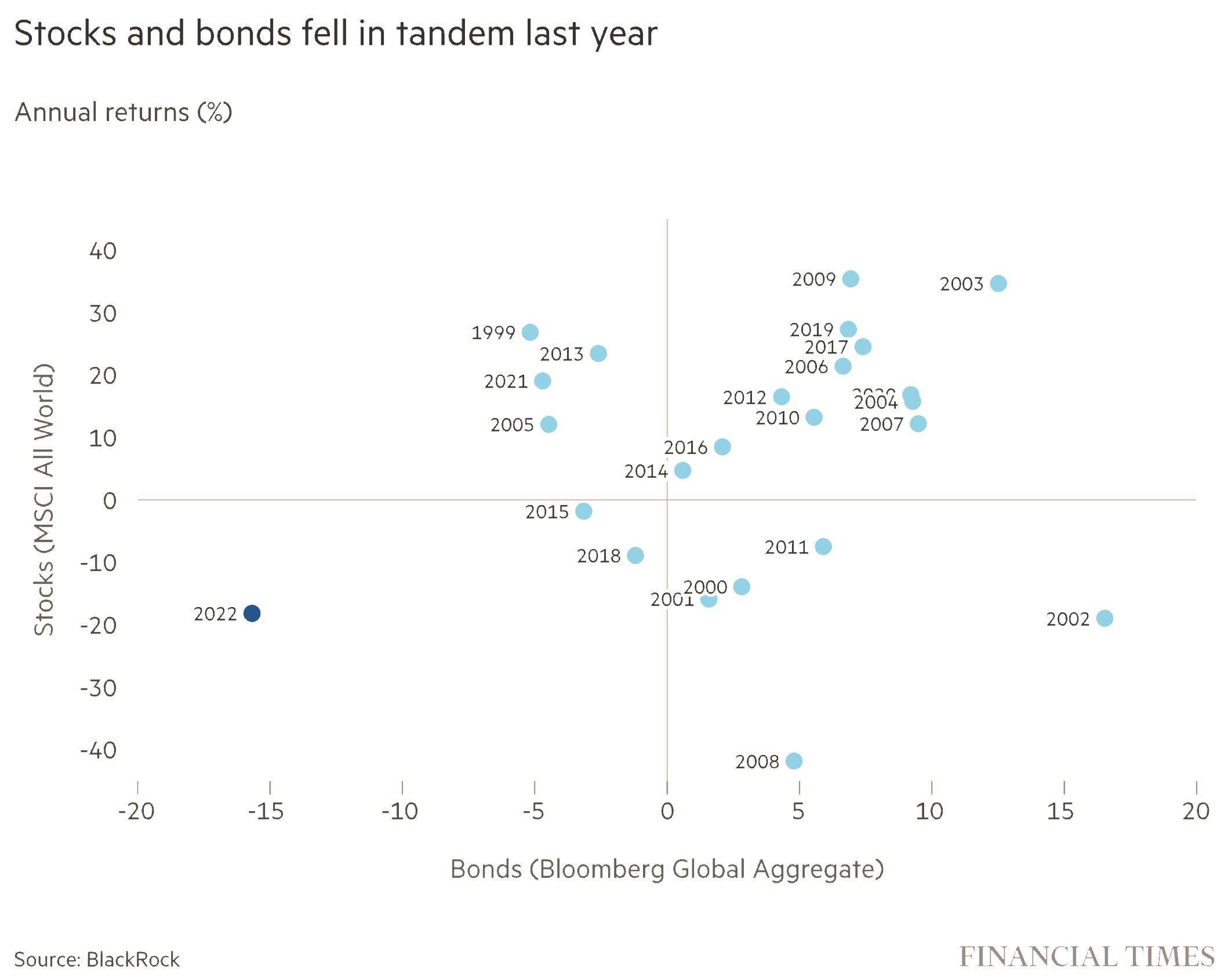

However, 2022 was a particularly terrible year for investors holding bonds, equities, or both, affecting almost all global investors; this has understandably resulted in concerns about the effectiveness of the 60/40 portfolio. The figure below illustrates how dramatic 2022 was for both stock and bond markets.

What Comes Next?

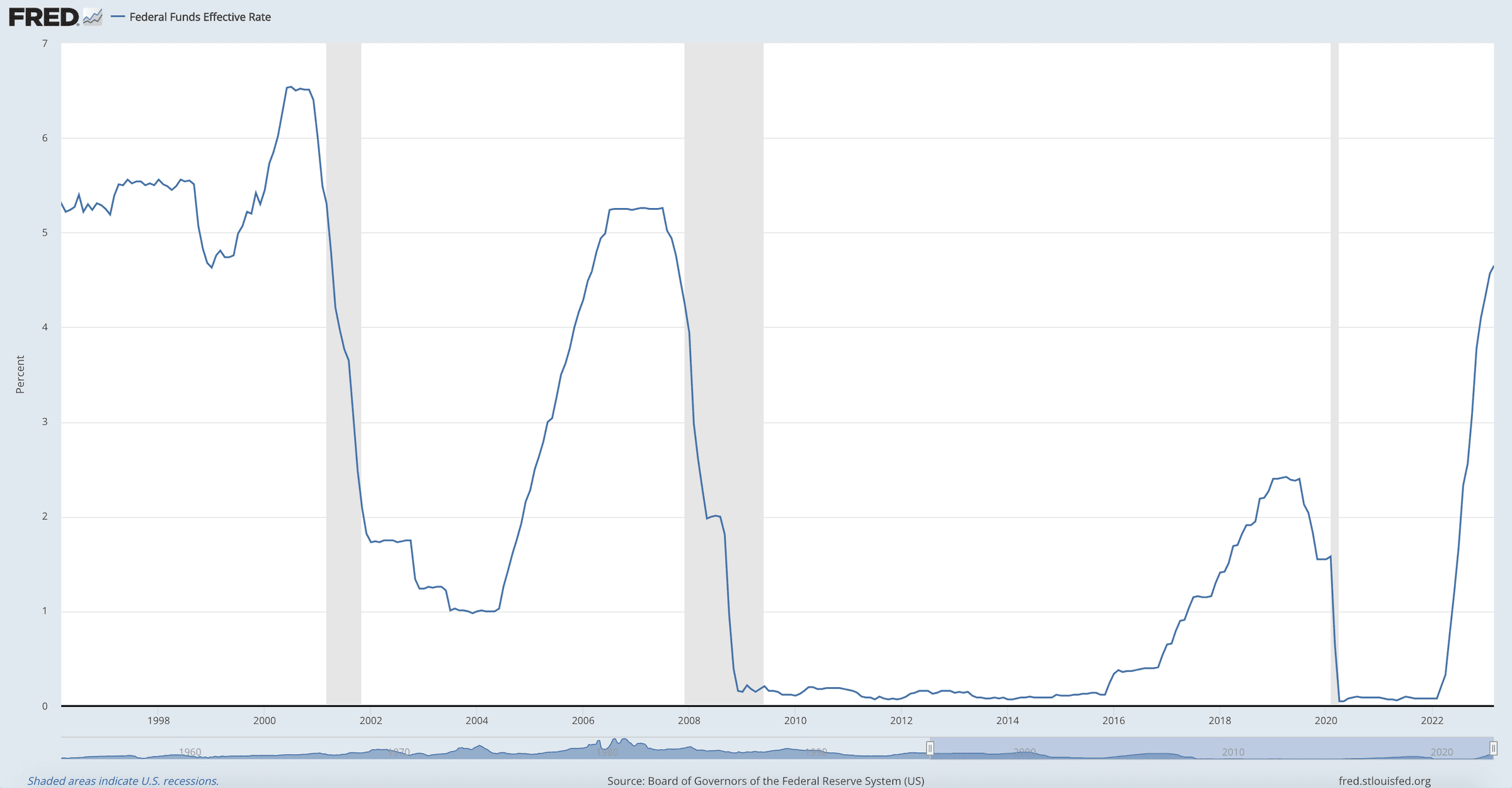

So with this in mind, let’s look at the federal funds rate chart since the mid-90s to determine whether this will persist:

The rapid increase in interest rates portrayed in 2022 was the main contributor to last year’s market performance for two reasons:

- A higher short-term interest rate makes all other investments less appealing by opportunity cost;

- The cost of lending for everyone has increased dramatically, making debt more expensive for companies and investors buying with leverage.

An important observation, that we will come back to later in the article, is that rates had also previously peaked in 2000 (6.5%) and 2007 (5.26%).

As for today, currently priced into the bond and equity market is a projection that interest rates will be 5.15% as of next week and continue to be for the summer (link).

If we revisit the first chart, we see that the bottom right quadrant are years when equity markets have declined dramatically, yet bonds have increased in value. These instances happened in both 2008 & 2002 when benchmark interest rates were at peaks.

The Most Disruptive Risks

In financial markets, it’s a common practice to identify and list the perceived risks likely to impact the market. However, the most commonly cited risks are often those that have already been factored into the market price. So, this can create a potential blind spot as the most disruptive risks are those people are not talking about or have not fully considered.

These risks may seem insignificant or go unnoticed until they surface, but they have the potential to impact the market significantly. We have seen this play out in the dot-com bubble, the Great Recession, and most recently with COVID-19. In such situations, the immediate policy response is to lower interest rates to protect the market, as previously evidenced in the charts. In such scenarios where previously held yields are no longer available, high-quality bonds are the primary beneficiaries when investors flock to safety.

The Takeaway

This is where the 60/40 portfolio comes into play, as it is designed to protect against such uncertainties. It has failed to be effective in 2022 where the main contributor to negative performance has been raising of rates. However, its effectiveness is optimized when interest rates are higher such as today and will outperform when interest rates inevitably head back down.

Frequently asked questions

Is 60/40 actually dead?

No — but it needs supplementation. Over multi-decade periods 60/40 has delivered solid risk-adjusted returns. The single year of 2022 (when both equities and bonds fell) was an outlier that exposed the strategy's vulnerability when correlations break. Adding alternatives addresses the gap without abandoning the framework.What's the modern equivalent of 60/40?

Closer to 50/30/20 — 50% equities, 30% fixed income, 20% alternatives — for HNW investors with appropriate liquidity tolerance. The alternatives sleeve (private credit, infrastructure, real assets) adds diversification that pure stock-bond mixes don't provide in stressed environments.Why did 2022 break 60/40?

Inflation and rapid rate hikes hit both asset classes simultaneously. Equities fell on multiple compression and growth concerns; bonds fell because rising rates directly reduce bond prices. The diversification benefit that normally protects 60/40 disappeared — both legs of the portfolio fell together.

Related reading

More on Portfolio construction

- InsightWhy Diversification Matters in a Fragile Global EconomyStagflation fears in the U.S. are rising, but your portfolio doesn't have to suffer. Learn why geographic diversification is essential for long-term resilience.

- InsightWhy Owning Everything WorksStop guessing the next winner. Discover why broad, global exposure across sectors, geographies, and asset classes delivers better risk-adjusted returns.

- FrameworkTwo Types of Risk: Tail-Side vs VolatilityUnderstand tail risk vs. volatility risk with VaultWealth. Learn how these distinct risks impact your investment strategy and long-term financial planning.